Roam Digital

Web3.0 & Vehicle Insurance

Role

UX Designer and Researcher

Skills

Research

UX Design

User Interviews

Duration

3 months

Tools

Figjam

Confluence

Jira

Context

IAG (Insurance Australian Group) is one of the biggest insurance companies in APAC. They wanted to understand how emerging WEB3.0 technology could impact and benefit the insurance industry. Our goal was to explore how this tech could solve problems in the automotive and insurance sectors.

We started with a kick-off meeting to understand the client's goals, what they already had, and how we would organize the project.

Kick-off meeting with the clients

Understanding and Exploring

In this phase, we gathered all IAG documents on customer insights, business models, strategies, and user journeys. We researched competitors and market solutions similar to what they wanted to achieve. We focused on two main areas:

The Tech

- Blockchain is the most known tech in the Web3 stack.

- We learned there are many types of blockchain, with multiple providers for each.

DeFi Insurance

- We analyzed existing decentralized insurance platforms to understand their strengths and weaknesses.

- We provided product owners with an informed and objective assessment of DeFi propositions.

Definition

“WEB 3.0 runs on infrastructure that no one person or entity owns.”

Users retain ownership of their data and benefit from any value created during transactions. We used our findings to explore possibilities, eliminate unfeasible ideas, and focus on the most promising ones. We held a workshop with IAG to define the problem statement, which anchored our thinking and guided our decisions.

Problem framing workshop with the clients

Problem Statement

Narrowing Things Down

We brainstormed ideas using the "How Might We" framework, leveraging IAG's market research and our own Web3.0 research. We then mapped the ecosystems of the most promising ideas to validate their feasibility.

Workshop to brainstorm opportunities using the "How Might We" framework

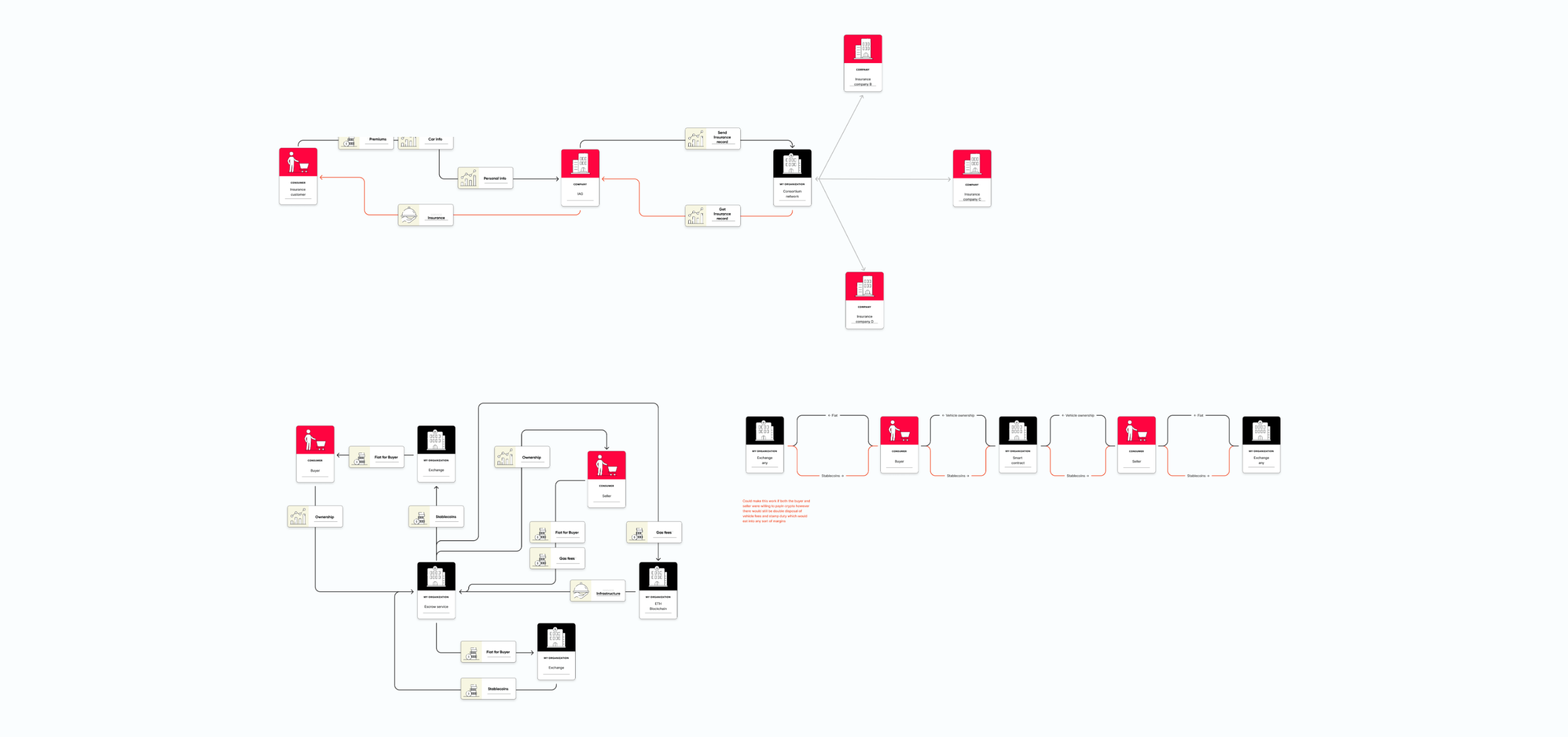

We mapped the ecosystems of the most promising ideas to understand the scope of a blockchain-based solution.

Ecosystem mapping to check feasibility of the ideas

A Fork in the Road

You're not the owner of your Web3 solution. Applying WEB3.0 tech to a problem IAG customers have either reduces or removes IAG's involvement and benefits.

Look at whom IAG are customers of and their internal problems to see if Web3.0 tech can serve them.

or

Understand what a decentralized insurance provider might look like and pose strategies to defend against it.

Understanding DeFi Insurance

Instead of creating an insurance product using Web3.0, we created a strategy plan to help IAG compete against those products. We assessed existing decentralized insurance platforms and made an informed and objective assessment of decentralized insurance propositions.

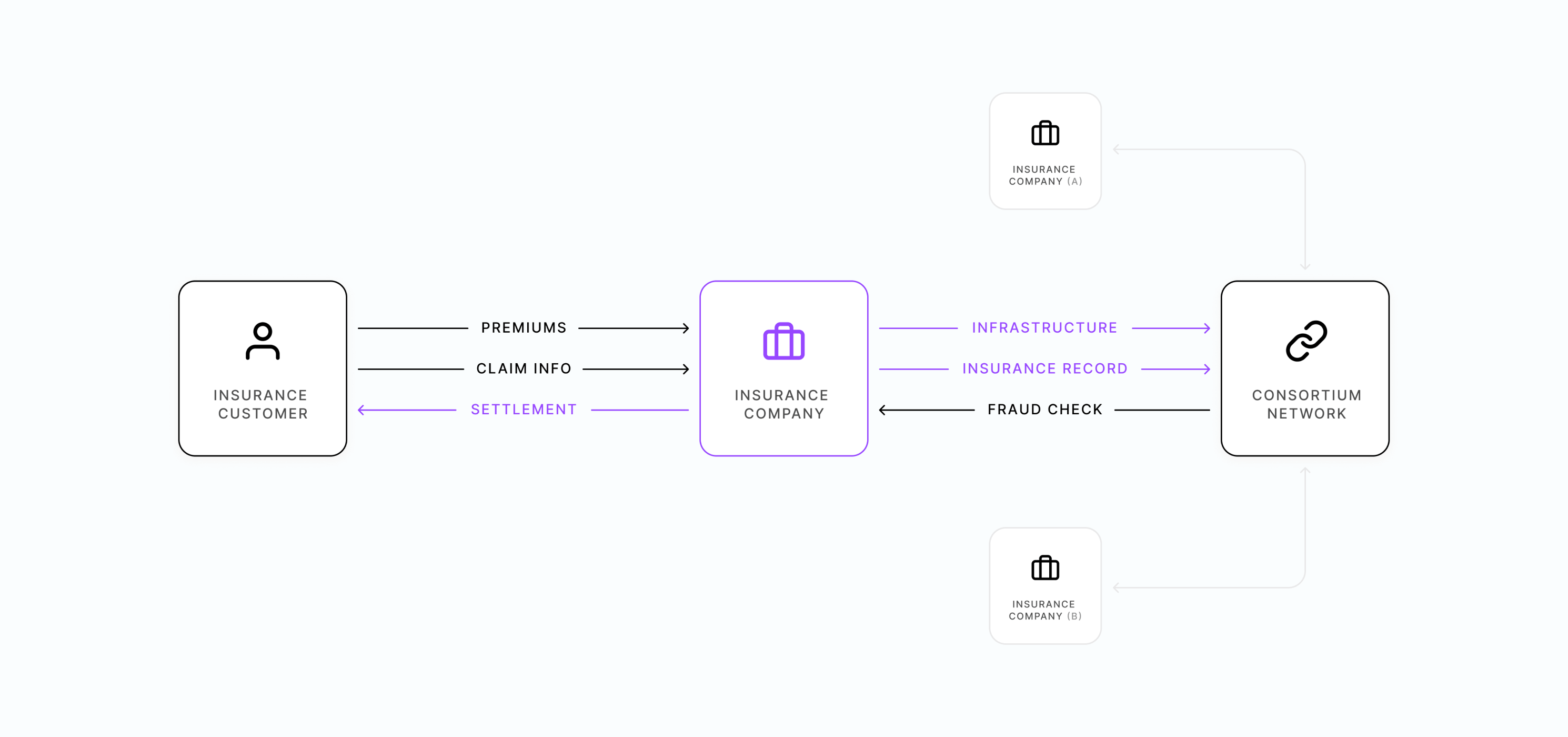

Traditional ecosystem of a car insurance company

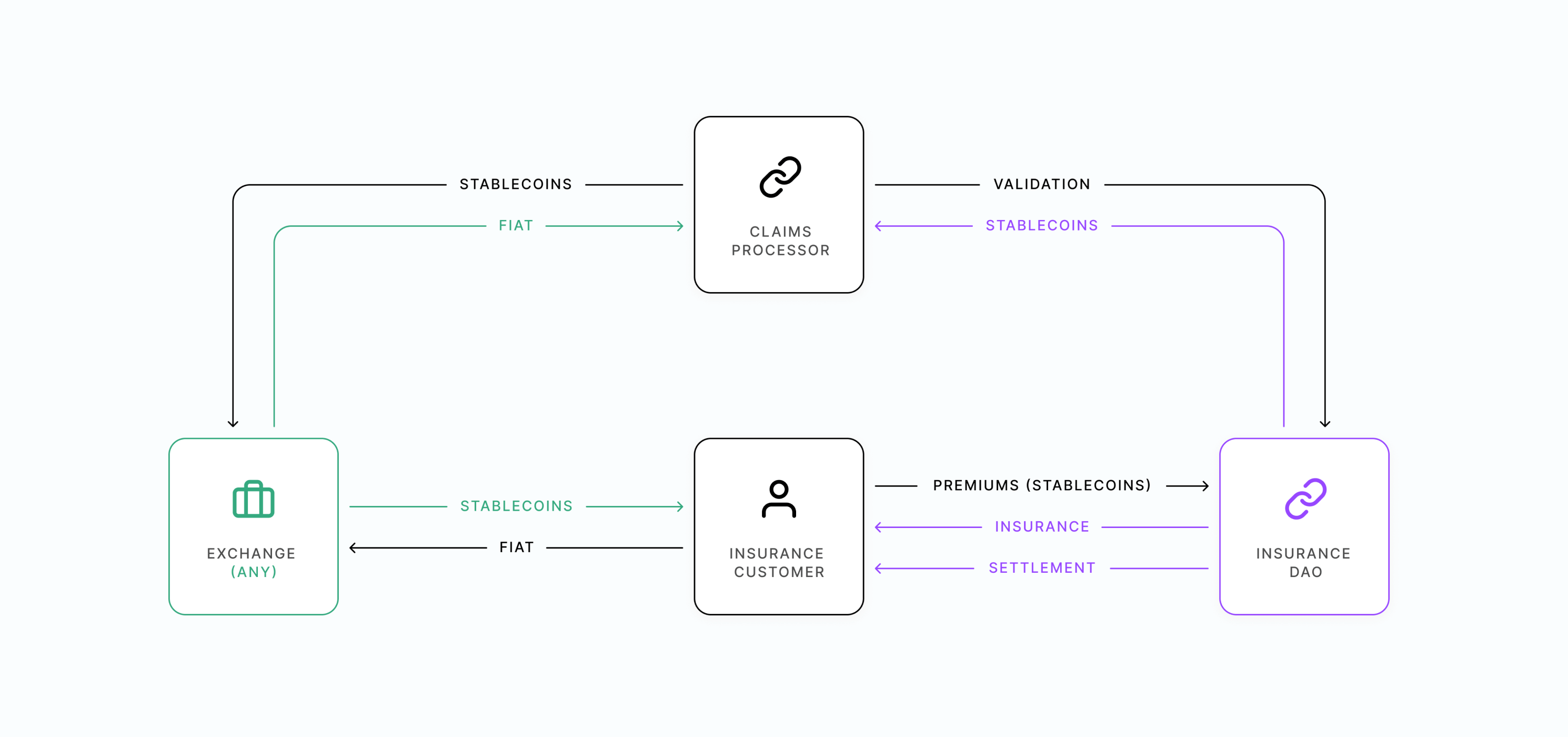

Decentralized ecosystem of this industry

Conclusion

Main Learnings about DeFi

Smart Contracts can automatically trigger when certain criteria are met, resulting in insurance payouts without needing to manually review every claim.

Automation of key transactions reduces running costs of the insurance product and can be passed on to customers as lower premiums.

DAO insurance products often adopt a Discretionary Mutual model. Members can participate in governance and many aspects of running the service, such as assessing new claims.

- Parametric risk with plenty of highly available, accurate, and independent data sources.

- When a specific risk is easy to articulate upfront.

- Occurrence of a risk event is easy to prove.

- Lack of consistent or dependable data sources.

- Occurrence of risk event is hard to prove without ambiguity.

- End up needing to manually review claims to weigh evidence and determine liability.

Solution

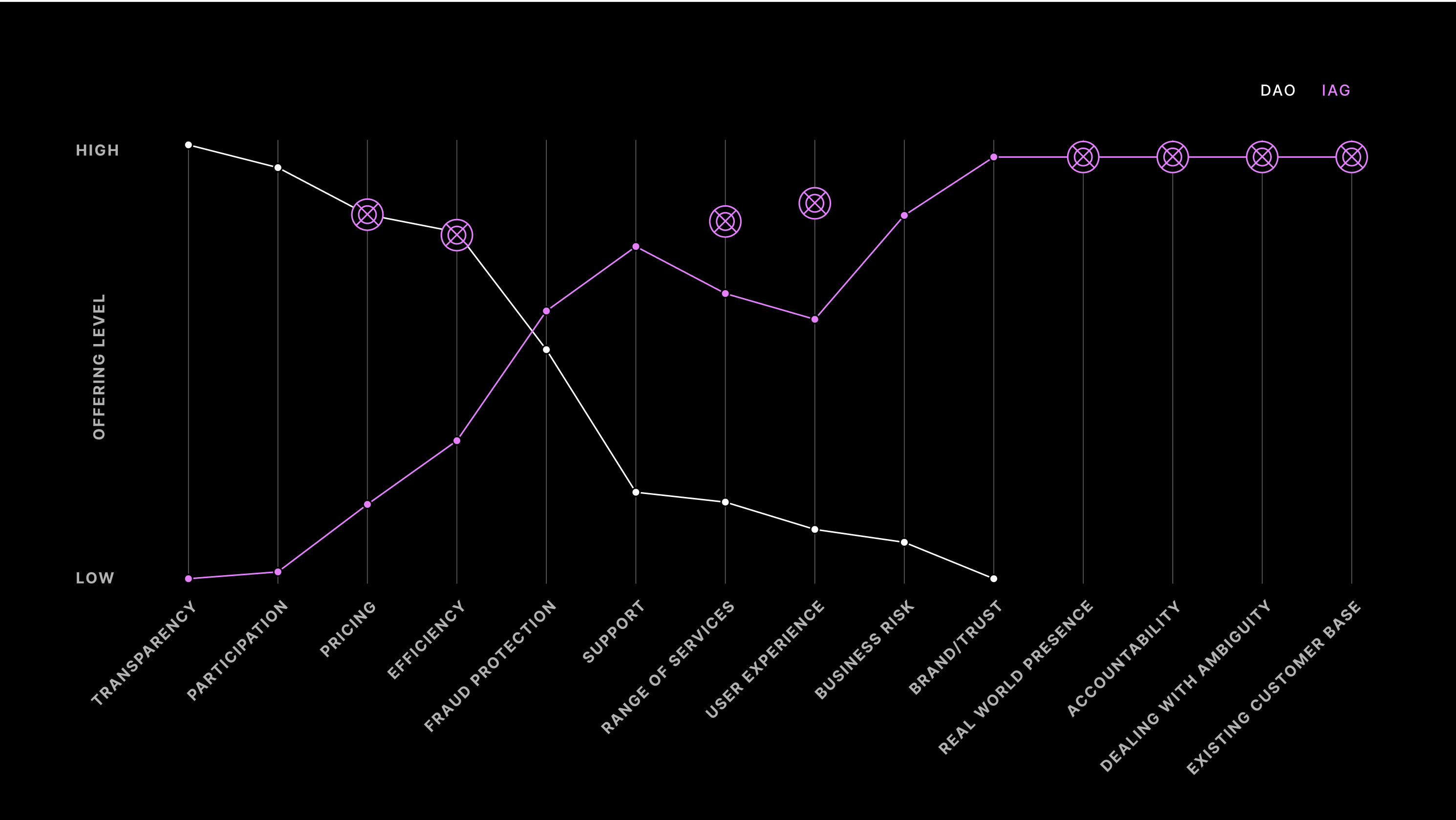

To prioritize strategy points for competing against a DeFi insurance company, we used the Blue Ocean Strategy framework with the IAG team, brainstorming competing points and evaluating strengths and weaknesses.

Blue Ocean Strategy

We developed several initiatives for each highlighted point.

Blue Ocean Strategy Canvas

The Challenges for DeFi Insurance Products

DeFi insurers need mass adoption of technology to realistically compete on price and efficiency. They may achieve a similar strategy using participants to vote, but it is harder to scale while maintaining a cost advantage.

Initiatives for scenarios where DeFi insurers overcome those challenges

- Investing in automation to compete on costs.

- Bundling parametric products with non-parametric products to build product costs.

- Lobbying to block DeFi insurers from being recognized by the government and creating a moat of regulation around products which are legally required.

Let's get in touch!

Feel free to reach out, I'm always up for a good chat :)

© Victor Zanivan 2026